Retirement Guide for Raytheon Employees

2024 Tax Changes and Inflation

Author

John Lynch - Senior Vice President, Financial Advisor CPWA® , CIMA ®

It is imperative for individuals to be aware of new changes made by the IRS. The main factors that will impact employees will be the following:

- The standard deduction for 2024 will rise to $21,900 for heads of household, $29,200 for joint filers, and $14,600 for single filers and married filers filing separately.

- Taxpayers may increase their standard deduction by an additional $1,550 if they are blind or over 65. That amount jumps to $1,950 if also unmarried or not a surviving spouse.

Contributions to retirement accounts: You can lower your tax liability by making contributions to your employer's 401(k) plan, and the maximum amount you can save has been raised for 2024. In 2024, the maximum contribution amount that individuals can make to their 401(k) plans will rise to $23,000, from $22,500 in 2023. Employees 50 years of age and older will be able to make catch-up contributions up to $7,500.

As a taxpayer who works for a corporation, you should be aware of the following significant changes regarding the Earned Income Tax Credit (EITC):

- The tax year 2024 maximum Earned Income Tax Credit amount is $7,830 for qualifying taxpayers who have three or more qualifying children, up from $7,430 for tax year 2023.

- Married taxpayers filing separately can qualify: You can claim the EITC as married filing separately if you meet other qualifications. This was not available in previous years.

Deduction for cash charitable contributions: The special deduction that permitted married couples filing jointly to deduct $600 and single non-temizers to deduct up to $300 in cash donations to eligible charities has expired.

Changes to the Child Tax Credit:

- The maximum tax credit per eligible child is $3,000 for those aged six to seventeen, and $2,000 for those under the age of five. Furthermore, unlike in 2023, you cannot obtain a portion of the credit beforehand.

- As a parent or guardian, you are eligible for the Child Tax Credit if your adjusted gross income is less than $200,000 when filing individually or less than $400,000 if you're filing a joint return with a spouse.

- A 70 percent, partial refundability affecting individuals whose tax bill falls below the credit amount.

2024 Tax Brackets

With rising prices for the same basket of goods, inflation gradually reduces purchasing power. You will need to account for increasing costs in your plan if you want to keep your retirement standard of living the same after you leave your company. In 2023, the rate of inflation shot up to 4.9%, a drastic increase from 2020's 1.4%. The Federal Reserve aims to maintain inflation at 2% annually. Even though costs have increased significantly overall, there are certain areas, like healthcare, to be mindful of if you are close to or already retired from your company.

When creating your comprehensive retirement plan from your company, it is imperative that you take all of these factors into account.

*Source: IRS.gov, Yahoo, Bankrate, Forbes

Recent Layoff Announcements & Other Raytheon News

Restructuring and Changes in Leadership: Raytheon's parent company, RTX, announced a major reorganization from four core divisions to three. With the merger with United Technologies Corp., this attempts to increase stability and streamline operations. Along with handling a crisis involving a defect in Pratt & Whitney's geared turbofan engine, the business is also avoiding possible spending ceilings on defense. (Sources: Defense News, Raytheon).

Blogs You May Enjoy:

![]()

Planning Your Raytheon Retirement

Retirement planning is a verb. And consistent action must be taken whether you’re 20 or 60.

The truth is that most Americans don’t know how much to save or the amount of income they’ll need.

No matter where you stand in the planning process, or your current age, we hope this guide gives you a good overview of the steps to take, and provides some resources that can help you simplify your transition into retirement and get the most from your benefits.

You know you need to be saving and investing, but you don’t have the time or expertise to know if you’re building retirement savings that can last.

"A separate study by Russell Investments, a large money management firm, came to a similar conclusion . Russell estimates a good financial advisor can increase investor returns by 3.75 percent."

Source: Is it Worth the Money to Hire a Financial Advisor?, the balance, 202

Starting to save as early as possible matters. Time on your side means compounding can have significant impacts on your future savings. And, once you’ve started, continuing to increase and maximize your 401(k) contributions is key, and can lead to huge windfalls later on in your life.

As decades go by, you’re likely full swing into your career, and your income probably reflects that. However, the challenges to saving for retirement start adding up: a mortgage, raising children and saving for their college.

One of the classic planning conflicts is saving for retirement, versus saving for college. Most financial planners will tell you that retirement should be your top priority, because your child can usually find support from financial aid while you’ll be on your own to fund your retirement.

Our recommendations for retirement savings always take into account your particular financial status and aspirations. Nonetheless, during your 30s and 40s, think about setting aside at least 10% of your income for retirement funds.

When you reach your 50s and 60s, you should be at the height of your earning potential and have some of your biggest expenses—like a mortgage or raising children—behind you or shortly in the rearview mirror. Now could be a good time to see whether you can increase your retirement savings target to 20% or higher of your income. This may be the last chance that many individuals have to put money down.

Employees who are 50 years of age or older in 2024 have the option to contribute up to $23,000 to their 401(k) or retirement plan. After they reach this cap, they can make additional $7,500 in catch-up payments, for a total annual contribution cap of $30,500. Every year, these caps are revised to account for inflation.

Over 50? You can invest up to $19,500 into your retirement plan / 401(k).

As you enter your 50s and 60s, you’re ideally at peak earning years with some of your major expenses, such as a mortgage or child-rearing, behind you or soon to be in the rearview mirror. This can be a good time to consider whether you have the ability to boost your retirement savings goal to 20% or more of your income. For many people, this could potentially be the last opportunity to stash away funds.

In 2022, workers aged 50 or older can invest up to $27,000 into their retirement plan / 401(k). Once they meet this limit, they can add an additional $6,500 in catch-up contributions. These limits are adjusted annually for inflation.

If you’re over 50, you may be eligible to use a catch-up contribution within your IRA.

Why are 401(k)s and matching contributions so popular?

These retirement savings vehicles give you the chance to take advantage of three main benefits:

- Compound growth opportunities (as seen above)

- Tax saving opportunities

- Matching contributions

Matching contributions are just what they sound like: your employer (in this case, Raytheon) matches your own 401(k) contributions with money that comes from the company. If Raytheon matches, the company money typically matches up to a certain percent of the amount you put in.

Unfortunately, many people don’t take full advantage of the employer match because they’re not putting in enough themselves.

$1,336 - A 2020 study from Financial Engines titled “Missing Out: How Much Employer 401(k) Matching Contributions Do Employees Leave on the Table?”, revealed that employees who don’t maximize the company match typically leave $1,336 of potential extra retirement money on the table each year.

- If Raytheon will match up to 3% of your plan contributions and you only contribute 2% of your salary, you aren’t getting the full amount of Raytheon's potential match.

- By bumping up your contribution by just 1%, Raytheon is now matching 3% (the max) of your contributions for a total contribution of 6% of your salary. You aren’t leaving money on the table.

Whether you live in the U.S. or Puerto Rico, you'll receive quite a bit of useful information from this article! Speak with a Raytheon-focused advisor by clicking the button below.

Whether you’re changing jobs or retiring, knowing what to do with your hard-earned retirement savings can be difficult. A plan sponsored by Raytheon, such as a pension and 401(k), may make up the majority of your retirement savings, but how much do you really know about that plan and how it works?

There are seemingly endless rules that vary from one retirement plan to the next, early out offers, interest rate impacts, age penalties, and complex tax impacts.

Increasing your investment balance and reducing taxes is the key to a successful retirement plan spending strategy. At The Retirement Group, we can help you understand how your Raytheon retirement scheme fits into your overall financial picture, and how to make that plan work for you.

Workers are far more likely to rely on their workplace defined contribution (DC) retirement plans as a source of income.

Getting help and leveraging the financial planning tools and resources Raytheon makes available can help you understand whether you are on track, or need to make adjustments to meet your long-term retirement goals...

Source: Schwab 401(k) Survey Finds Savings Goals and Stress Levels on the Rise

Raytheon Salaried Pension Plan

Raytheon Technologies offers a comprehensive pension plan, known as the Raytheon Salaried Pension Plan, which combines a traditional pension formula and a cash balance formula starting in 2023. This hybrid approach ensures employees receive retirement income based on years of service, salary, and performance.

Eligibility

To be eligible for Raytheon's pension plan:

Employment Requirements: Most full-time employees are eligible for the pension plan after meeting minimum service requirements.

Hire Date: Heritage Raytheon employees hired before January 1, 2007, who remain actively employed as of January 1, 2023, are covered under this plan.

Vesting: Employees are fully vested after three years of service, meaning they have a guaranteed right to receive the benefits they’ve earned(RTX Fact Sheet (401k)).

How the Pension Plan Works

The pension plan has two components:

Traditional Defined Benefit Formula (Until Dec. 31, 2022): Employees earn a pension based on a formula that considers years of service and final average earnings. This portion of the pension is calculated as a lifetime annuity.

Cash Balance Formula (Starting Jan. 1, 2023): After 2022, the pension converts to a cash balance plan. In this formula, Raytheon credits an account for each eligible employee with both pay credits (based on the employee's age and salary) and interest credits (based on long-term Treasury bond yields). This account balance grows over time, and employees can choose to take it as a lump sum or convert it into a lifetime annuity upon retirement.

Pension Calculation Example

To provide an example calculation, let’s consider an employee with the following details:

Years of Service (pre-2023): 20 years

Final Average Salary: $100,000

Traditional Pension Benefit: Based on the old formula, if the multiplier is 1.5%, the pension calculation would be:

Traditional Pension = 20 × 100,000 × 0.015 = $30,000 annually

This amount is typically paid as a monthly annuity of $2,500.

For the cash balance portion (post-2023), if the employee's pay credit is 4% of salary and they have two years of service under this formula, the cash balance would be:

Pay Credits: $100,000 × 0.04 × 2 = $8,000

Interest Credits: Assuming a 3% interest credit per year, the cash balance would increase by 3% annually.

The total cash balance after two years would be approximately $8,500 with interest.

Raytheon’s pension plan provides a robust retirement option for eligible employees, offering traditional pension benefits for pre-2023 service and a cash balance formula for post-2023 service. Employees can take advantage of both monthly annuities and lump sum payouts depending on their preferences at retirement.

Lump-Sum vs. Annuity

Retirees who are eligible for a pension are often offered the choice of receiving their pension payments for life, or receive a lump-sum amount all-at-once. The lump sum is the equivalent present value of the monthly pension income stream – with the idea that you could then take the money (rolling it over to an IRA), invest it, and generate your own cash flow by taking systematic withdrawals throughout your retirement years.

The upside of electing the monthly pension is that the payments are guaranteed to continue for life (at least to the extent that the pension plan itself remains in place and solvent and doesn’t default). Thus, whether you live 10, 20, 30, or more years after retiring from your company, you don’t have to worry about the risk of outliving the monthly pension.

The major downside of the monthly pension are the early and untimely passing of the retiree and joint annuitant. This often translates into a reduction in the benefit or the pension ending altogether upon the passing. The other downside, it that, unlike Social Security, company pensions rarely contain a COLA (Cost of Living Allowance). As a result, with the dollar amount of monthly pension remaining the same throughout retirement, it will lose purchasing power when the rate of inflation increases.

In contrast, selecting the lump-sum gives you the potential to invest, earn more growth, and potentially generate even greater retirement cash flow. Additionally, if something happens to you, any unused account balance will be available to a surviving spouse or heirs. However, if you fail to invest the funds for sufficient growth, there’s a danger that the money could run out altogether and you may regret not having held onto the pension’s “income for life” guarantee.

Ultimately, the “risk” assessment that should be done to determine whether or not you should take the lump sum or the guaranteed lifetime payments that your company pension offers, depends on what kind of return must be generated on that lump-sum to replicate the payments of the annuity. After all, if it would only take a return of 1% to 2% on that lump-sum to create the same monthly pension cash flow stream, there is less risk that you will outlive the lump-sum. However, if the pension payments can only be replaced with a higher and much riskier rate of return, there is, in turn, a greater risk those returns won’t manifest and you could run out of money.

Your Raytheon 401(k) Plan

Raytheon Savings and Investment Plan (RAYSIP)

The Raytheon Savings and Investment Plan (RAYSIP), a 401(k) savings plan offered by Raytheon Technologies Corporation, assists staff members in setting aside money for retirement. Employees may fund their retirement accounts with pre-tax or Roth after-tax contributions under the terms of the plan. Raytheon will match employee contributions up to a certain amount. Here’s a detailed overview:

Eligibility

Most full-time and part-time employees of Raytheon are eligible to participate in RAYSIP after completing a short waiting period, typically around 30 days of employment. Eligibility criteria include:

Full-time employees: Automatically eligible after the waiting period.

Part-time employees: Eligibility may depend on hours worked.

Exclusions: Unionized employees and certain classifications, such as those working for Raytheon subsidiaries like Puerto Rico operations, may be excluded from RAYSIP(RTX Fact Sheet (401k)).

Contributions

Employees may fund their 401(k) account with a portion of their bonuses, base pay, and other qualifying income. The maximum contribution allowed is subject to IRS limits, which for 2024 is $23,000, with an additional $7,500 catch-up contribution for employees aged 50 and older.

Raytheon matches employee contributions up to a specific percentage:

100% match on the first 4% of employee contributions.

RAYSIP contributions: In addition to matching, Raytheon may provide employer contributions as a percentage of pay based on age and service.

Vesting

Vesting is the period of time that a worker at Raytheon has to work before they are entitled to all of the matching contributions made by the business. Raytheon’s RAYSIP offers full vesting in company contributions after three years of service. This means employees are entitled to all the company contributions if they stay employed with Raytheon for at least three years.

Example Calculation

Let’s assume an employee earns $100,000 annually and contributes 6% of their salary to the 401(k) plan.

Employee Contribution: Employee Contribution = $100,000 × 0.06 = $6,000

Company Match: Raytheon matches 100% of the first 4% of the employee’s contribution.

Company Match = $100,000 × 0.04 = $4,000

Total Contribution: Total Contribution = $6,000 (employee) + $4,000 (company match) = $10,000

In this example, the employee contributes $6,000, and Raytheon contributes $4,000, bringing the total annual contribution to $10,000.

For the most accurate information, employees should consult Raytheon’s official 401(k) plan documents or contact the company’s HR department.

Benefits of RAYSIP

Tax Benefits: Employee contributions reduce taxable income (pre-tax) or grow tax-free (Roth contributions).

Investment Choices: Employees can choose from a range of investment options, including mutual funds, company stock, and other asset classes.

Additional Contributions: Raytheon also provides additional contributions based on age and service under the Raytheon Investment Savings Plan (RISP), further increasing employee retirement savings.

More than half of plan members acknowledge they lack the knowledge, interest, or time necessary to manage their 401(k) investments. But the benefits of getting help goes beyond convenience. Studies like this one, from Charles Schwab, show those plan participants who get help with their investments tend to have portfolios that perform better: The annual performance gap between those who get help and those who do not is 3.32% net of fees. This means a 45-year-old participant could see a 79% boost in wealth by age 65 simply by contacting an advisor. That’s a pretty big difference.

Getting help can be the key to better results across the 401(k) board.

A Charles Schwab study found several positive outcomes common to those using independent professional advice. They include:

- Improved savings rates – 70% of participants who used 401(k) advice increased their contributions.

- Increased diversification – Participants who managed their own portfolios invested in an average of just under four asset classes, while participants in advice-based portfolios invested in a minimum of eight asset classes.

- Increased likelihood of staying the course – Getting advice increased the chances of participants staying true to their investment objectives, making them less reactive during volatile market conditions and more likely to remain in their original 401(k) investments during a downturn. Don’t try to do it alone. Get help with your company's 401(k) plan investments. Your nest egg will thank you.

Raytheon Stock Ownership Plan (RAYSOP)

Raytheon Technologies Corporation offered the Raytheon Stock Ownership Plan (RAYSOP) as a component of their Raytheon Savings and Investment Plan (RAYSIP). This plan provided eligible employees with company contributions to a Raytheon Stock Fund. Although active contributions to RAYSOP were discontinued after 2005 for most employees, it remains a crucial part of Raytheon’s legacy benefits structure for long-term employees.

Eligibility

Eligibility for RAYSOP was historically based on the following factors:

Full-time and Part-time Employees: Most employees who were hired before 2005 and had an active RAYSIP account were eligible to receive contributions to the Raytheon Stock Fund.

Employment Requirements: After 2005, contributions to RAYSOP ceased for most employees except those covered under specific collective bargaining agreements, who continued receiving contributions.

Program Structure

The structure of RAYSOP allowed Raytheon to make contributions to the Raytheon Stock Fund within RAYSIP accounts. These contributions were based on the employee’s performance and other company-specific metrics. Employees became shareholders of Raytheon by holding stock within the Raytheon Stock Fund, granting them the ability to vote on company matters and receive dividends from their shares.

For eligible employees, Raytheon’s contributions to the stock fund represented a valuable long-term investment. The contributions were vested based on standard vesting rules within the RAYSIP plan.

Vesting and Contributions

Vesting: Employees were fully vested in their contributions and any matching contributions to the RAYSOP component based on the vesting schedule of the broader RAYSIP plan. For most employees, this meant becoming fully vested after three years of service.

Discontinuation: For most employees, contributions to RAYSOP ended in March 2005, and any remaining funds in the Raytheon Stock Fund were left to grow based on market performance.

Example Calculation

Let’s assume an employee had a balance of $50,000 in the Raytheon Stock Fund as of 2005 when contributions stopped, and the fund’s average growth rate was 7% per year.

Initial Balance: $50,000

Annual Growth: 7%

Duration: 15 years (from 2005 to 2020)

The future value of the stock fund after 15 years would be calculated using the formula for compound interest:

Future Value = 50,000 × (1+0.07)15 = 50,000 × (2.759) = $137,950

Thus, the employee's Raytheon Stock Fund would grow to approximately $137,950 after 15 years at an average annual growth rate of 7%.

The information provided here is based on historical data from Raytheon’s benefits documents and the structure of the RAYSIP plan, including contributions to the Raytheon Stock Fund. The example calculation assumes a standard growth rate for illustrative purposes and does not account for fluctuations in the stock market or dividend reinvestment specifics.

For precise details, employees should consult Raytheon’s benefits documents or contact their HR department for current policies .

In-Service Withdrawals

Generally speaking, you can withdraw amounts from your account while still employed under the circumstances described below.

It’s important to know that certain withdrawals are subject to regular federal income tax and, if you’re under age 59½, you may also be subject to an additional 10% penalty tax. You can determine if you’re eligible for a withdrawal, and request one, online or by calling the Raytheon Benefits Center.

Rolling Over Your 401(k)

As long as the plan participant is younger than age 72, an in-service distribution can be rolled over to an IRA. A direct rollover would avoid the 10% early withdrawal penalty as well as the mandatory 20% tax withholding. Your plan summary outlines more information and possible restrictions on rollovers and withdrawals.

Because a withdrawal permanently reduces your retirement savings and is subject to tax, you should always consider taking a loan from the plan instead of a withdrawal to meet your financial needs. Unlike withdrawals, loans must be repaid, and are not taxable (unless you fail to repay them). In some cases, as with hardship withdrawals, you are not allowed to make a withdrawal unless you have also taken out the maximum available plan loan.

You should also know that the plan administrator reserves the right to modify the rules regarding withdrawals at any time, and may further restrict or limit the availability of withdrawals for administrative or other reasons. All plan participants will be advised of any such restrictions, and they apply equally to all employees.

Borrowing from your 401(k)

Should you? Maybe you lose your job, have a serious health emergency, or face some other reason that you need a lot of cash. Banks make you jump through too many hoops for a personal loan, credit cards charge too much interest, and … suddenly, you start looking at your 401(k) account and doing some quick calculations about pushing your retirement off a few years to make up for taking some money out.

We understand how you feel: It’s your money, and you need it now. But, take a second to see how this could adversely affect your retirement plans.

Consider these facts when deciding if you should borrow from your 401(k). You could:

Lose growth potential on the money you borrowed.

Deal with repayment and tax issues if you leave your employer.

Repayment and tax issues, if you leave your employer.

Net Unrealized Appreciation (NUA)

When you qualify for a distribution, you have three options:

- Roll-over your qualified plan to an IRA and continue deferring taxes.

- Take a distribution and pay ordinary income tax on the full amount.

- Take advantage of NUA and reap the benefits of a more favorable tax structure on gains.

How does Net Unrealized Appreciation work?

An employee must first be qualified to receive benefits from a qualifying company-sponsored plan. The employee often accepts a "lump-sum" payout from the plan, disbursing all assets over the course of a year, upon retirement or reaching age 59 1⁄2. You can roll over the mutual fund and other investment portion of the plan into an IRA to further avoid taxes. After that, the highly valued firm stock is moved to an account that isn't for retirement.

When you move business shares from a tax-deferred account to a taxable account, you will receive a tax benefit. You currently apply NUA and are liable for ordinary income tax on the stock's cost base alone. The stock's increased value over its base is taxed at the lower long-term capital gains rate, which is now 15%, rather than the higher regular income tax. This could result in savings of more than 30%.

Would you be interested in speaking with a financial advisor from The Retirement Group one-on-one for a complimentary one-on-one session to learn more about NUA?

IRA Withdrawal

IRAs, 401(k)s, taxable funds, and other retirement accounts may be among your Raytheon retirement assets.

How therefore should you use your retirement income to maximize efficiency?

Instead of first taking money out of tax-deferred funds, you might want to think about using taxable accounts to cover your income needs in retirement. Your retirement funds may last longer as a result of this since they might grow tax-deferred. It is also necessary to schedule the required minimum distributions (RMDs) from traditional or rollover IRA accounts, as well as from any employer-sponsored retirement plans. This is because the IRS will be requiring, starting in 2020, that you start taking withdrawals from these kinds of accounts when you turn 72. The IRS may impose a 50% penalty on the amount you should have taken if you don't.

A new law permits anyone who turned 70½ before the end of 2019 to begin taking their RMDs on April 1 of the following year, when they turn 72.

Your IRA has two options for flexible distribution.

You have a few options when it comes to using your IRA to make money or to collect your required minimum distributions. Whichever option you select, IRA distributions are taxable on your income and, if you're under59½, may also be subject to penalties and other requirements.

Partial withdrawals: You can take out any quantity from your IRA whenever you want. By the time you turn 72, you will need to withdraw enough money from one or more IRAs to cover your annual required minimum distribution (RMD).

Systematic withdrawal plans: Set up recurring, automated withdrawals from your IRA at the frequency and amount that best suits your needs for retirement income. If your withdrawal plan does not comply with Code Section 72(t) regulations, you may be liable to an early withdrawal penalty of 10% if you are under 59½.

You can establish a systematic withdrawal strategy, ascertain RMD obligations, compute RMDs, and comprehend distribution choices with the assistance of your tax advisor.

Your Raytheon Benefits

The benefits offered by Raytheon Technologies Corporation to its staff members are extensive and include financial protection choices, wellness initiatives, health insurance, and retirement plans. These benefits encourage financial, emotional, and physical well-being in an effort to support workers and their families.

Qualifications

Benefit eligibility at Raytheon is often determined by length of service and employment status, such as full- or part-time work. Benefits are available to the majority of full-time and part-time workers, and they usually start on the first of the month after the employee's employment date. The entire range of benefits may not be available to contract or temporary workers, but eligibility varies by employment and area.

Key Benefits: Comprehensive health insurance policies, covering medical, dental, and vision care, are offered by Raytheon. These plans, which provide a range of deductibles and premium levels to suit the needs of employees and their families, may include PPOs, HMOs, and high-deductible health plans with health savings accounts (HSAs).

Retirement Savings programs: For qualified employees, Raytheon provides a number of retirement programs, such as the Raytheon Savings and Investment Plan (RAYSIP) and a regular pension plan. With RAYSIP, employees can fund their 401(k) plan with pre-tax or Roth after-tax monies, and Raytheon will match those contributions up to a predetermined proportion of the employee's salary. Heritage Raytheon employees are eligible for the pension plan, which will change to a cash balance formula in 2023 for those who meet the requirements.

Life and Disability Insurance: Raytheon offers choices for additional life insurance for employees and their dependents in addition to company-paid life insurance. Options for both short-term and long-term disability insurance are offered to safeguard employees' salaries in the event of illness or accident.

Paid Time Off: Workers are entitled to paid holidays, sick days, and personal time in addition to accruing vacation time based on their duration of service. Adoptive parents can also take use of parental leave, in addition to biological parents.

Wellness Programs: Raytheon provides employee assistance programs (EAPs), fitness challenges, and mental health resources. The general productivity and well-being of employees are the goals of these programs.

Tuition Reimbursement: Raytheon offers financial assistance for continuing education by covering the cost of job-related training and degree programs in order to promote professional development.

The data shown here is derived from official benefits documents and other internal sources, as well as general summaries of Raytheon's benefits offerings.

HSAs

Health Savings Accounts (HSAs) are frequently praised for helping people with high-deductible health plans manage their medical costs. Beyond only controlling medical costs, HSAs offer advantages over more conventional retirement plans such as 401(k)s. This is especially true if employer matching contributions have been fully utilized.

Recognizing HSAs

Individuals with high-deductible health insurance policies can open tax-advantaged accounts called Health Savings Accounts (HSAs). High-deductible plans are those that have a minimum deductible of $1,600 for single people and $3,200 for families as of 2024, according to the IRS. Triple tax benefits are offered by HSAs, which permit pre-tax contributions, tax-free investment growth, and tax-free withdrawals for approved medical costs.

HSA yearly contribution caps for 2024 are $4,150 for singles and $8,300 for families, plus an extra $1,000 for those 55 years of age and above. HSA funds, in contrast to those in Flexible Spending Accounts (FSAs), accrue and are carried over for an unlimited period of time.

Evaluating HSAs and 401(k)s After Matching

Contributions beyond the employer's maximum match in a 401(k) result in less immediate financial rewards. HSAs can serve as a strategic supplement in this situation. 401(k)s provide tax-deductible contributions and tax-deferred growth, but withdrawals are subject to taxes. In contrast, health savings accounts (HSAs) offer tax-free withdrawals for medical costs, which account for a sizeable amount of retirement spending.

HSA as a Tool for Retirement

The HSA shows its strength as a powerful retirement tool after age 65. The money can be taken out for anything, with the exception of ordinary income tax if it is used for non-medical costs. This flexibility is comparable to that of typical retirement plans, plus it comes with the bonus of tax-free withdrawals for medical bills, which is quite helpful considering the rising cost of healthcare in retirement.

Moreover, unlike Traditional IRAs and 401(k)s, HSAs do not have Required Minimum Distributions (RMDs), giving investors greater flexibility when it comes to retirement tax planning. Because of this, HSAs are especially beneficial for people who wish to reduce their taxable income or who may not need to access their savings right away when they retire.

HSA Investment Strategy

First, you should invest in an HSA cautiously, making sure that there are enough liquid assets to pay for short-term deductibles and other out-of-pocket medical costs. But after a safety net is in place, investing in a diverse range of equities and bonds and managing the HSA like a retirement account can greatly increase the account's long-term growth potential.

Making Use of HSAs in Retirement

HSAs can pay for a variety of retirement-related expenses:

Healthcare Costs Before Medicare: HSAs Can Cover Medical Expenses to Help You Become Enrolled in Medicare Healthcare Costs After Medicare: Medicare premiums and out-of-pocket medical expenses, such as dental and vision care, which are frequently not covered by Medicare, can be paid with HSAs.

Long-term Care: The money can be used to pay insurance premiums and for appropriate long-term care services.

Non-Medical Expenses: HSA funds may be withdrawn for non-medical costs up to the age of 65 without penalty, although income tax is due on these withdrawals.

In summary

In conclusion, after the advantages of 401(k) matching are fully realized, HSAs can be a better option for retirement savings due to their special advantages. Because of their tax benefits and flexibility in using funds, health savings accounts (HSAs) are a crucial part of an all-encompassing retirement plan. People can optimize their retirement financial health and ensure their medical and financial security by carefully controlling their contributions and withdrawals.

What Happens If Your Employment Ends

Your life insurance coverage and any optional coverage you purchase for your spouse/domestic partner and/or children ends on the date your employment ends, unless your employment ends due to disability. If you die within 31 days of your termination date, benefits are paid to your beneficiary for your basic life insurance, as well as any additional life insurance coverage you elected.

Note:

- You may have the option to convert your life insurance to an individual policy or elect portability on any optional coverage.

- If you stop paying supplementary contributions, your coverage will end.

- If you are at least 65 and you pay for supplemental life insurance, you should receive information in the mail from the insurance company that explains your options.

- Make sure to update your beneficiaries. See the Raytheon SPD for more details.

Beneficiary Designations

As part of your retirement and estate planning, it’s important to name someone to receive the proceeds of your benefits programs in the event of your death. That’s how Raytheon will know whom to send your final compensation and benefits. This can include life insurance payouts and any pension or savings balances you may have.

Next Step:

When you retire, make sure that you update your beneficiaries. Raytheon has an Online Beneficiary Designation form for life events such as death, marriage, divorce, child birth, adoptions, etc.

If you are unsure about Raytheon benefits, schedule a call to speak with one of our Raytheon-focused advisors

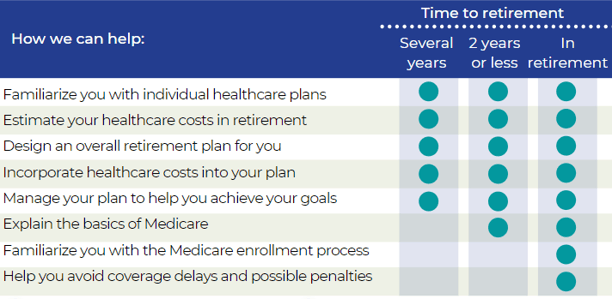

Social Security & Medicare

For many retirees, understanding and claiming Social Security can be difficult but identifying optimal ways to claim Social Security is essential to your retirement income planning. Social Security benefits are not designed to be the sole source of your retirement income, but a part of your overall withdrawal strategy.

Knowing the foundation of Social Security, and using this knowledge to your advantage, can help you claim your maximum benefit.

It’s your responsibility to enroll in Medicare parts A and B when you first become eligible — and you must stay enrolled to have coverage for Medicare-eligible expenses. This applies to your Medicare eligible dependents as well.

You should know how your retiree medical plan choices or Medicare eligibility impact your plan options. Before you retire, contact the U.S. Social Security Administration directly at 800-772-1213, call your local Social Security Office or visit ssa.gov .

They can help determine your eligibility, get you and/or your eligible dependents enrolled in Medicare or provide you with other government program information. For more in-depth information on Social Security, please call us.

Check the status of your Social Security benefits before you retire. Contact the U.S. Social Security Administration, your local Social Security office, or visit ssa.gov.

Are you eligible for Medicare, or will be soon?

If you or your dependents are eligible after you leave Raytheon, Medicare generally becomes the primary coverage for you or any of your dependents as soon as they are eligible for Medicare. This will affect your company-provided medical benefits.

You and your Medicare-eligible dependents must enroll in Medicare Parts A and B when you first become eligible. Medical and MH/SA benefits payable under the Raytheon-sponsored plan will be reduced by the amounts Medicare Parts A and B would have paid whether you actually enroll in them or not.

For details on coordination of benefits, refer to your summary plan description.

If you or your eligible dependent don’t enroll in Medicare Parts A and B, your provider can bill you for the amounts that are not paid by Medicare or your Raytheon-specific medical plan … making your out-of-pocket expenses significantly higher.

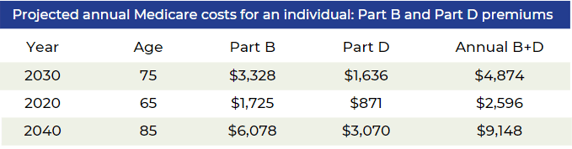

The Employee Benefit Research Institute (EBRI) estimates that Medicare will only pay for roughly 60% of a person's medical costs. With average prescription drug costs for their age, a 65-year-old couple will require $259,000 in savings to have a 90% chance of covering their medical expenses. A single woman will require $140,000 due to her longer life expectancy, while a single man will require $124,000.

Check your plan summary to see if you’re eligible to enroll in Medicare Parts A and B.

If you become Medicare-eligible for reasons other than age, you must contact the Raytheon benefit center about your status. *Source: Raytheon Summary Plan Description

Divorce

For 28% of couples over 50, the ideals of "happily ever after" and "til death do us part" will never come true. Most couples have saved together for decades, assuming all along that they would retire together. After a divorce, they face the expenses of a pre-or post-retirement life, but with half their savings (or even less).

If you’re divorced or in the process of divorcing, your former spouse(s) may have an interest in a portion of your retirement benefits. Before you can start your pension — and for each former spouse who may have an interest — you’ll need to provide Raytheon with the following documentation:

- A copy of the court-filed Judgment of Dissolution or Judgment of Divorce along with any Marital Settlement Agreement (MSA)

- A copy of the court-filed Qualified Domestic Relations Order (QDRO)

If Raytheon requests any documentation, send it to them in order to prevent your pension benefit from being suspended or delayed. To find out more information on strategies if divorce is affecting your retirement benefits, please give us a call.

You’ll need to submit this documentation to your company’s online pension center regardless of how old the divorce or how short the marriage. *Source: The Retirement Group, “Retirement Plans - Benefits and Savings,” U.S. Department of Labor, 2019; “Generating Income That Will Last Throughout Retirement,” Fidelity, 2019

Social Security and Divorce You can apply for a divorced spouse’s benefit if the following criteria are met:

You’re at least 62 years of age.

You were married for at least 10 years prior to the divorce.

You are currently unmarried.

Your ex-spouse is entitled to Social Security benefits.

The amount of your spousal benefit, which is half of your former spouse's full benefit amount if they were to claim it at full retirement age (FRA), is greater than your own Social Security benefit. Unlike with a married couple, your ex-spouse doesn’t have to have filed for Social Security before you can apply for your divorced spouse’s benefit, but this only applies if you’ve been divorced for at least two years and your ex is at least 62 years of age. If the divorce was less than two years ago, your ex must already be receiving benefits before you can file as a divorced spouse.

Unlike with a married couple, your ex-spouse doesn’t have to have filed for Social Security before you can apply for your divorced spouse’s benefit.

Divorce doesn’t even disqualify you from survivor benefits. You can claim a divorced spouse’s survivor benefit if the following are true:

Your ex-spouse is deceased

You are at least 60 years of age

You were married for at least 10 years prior to the divorce

You are single (or you remarried after age 60)

In the process of divorcing?

You remain married even if your divorce is not finalized by the time you retire. You have two options:

- Retire before your divorce is final and elect a joint pension of at least 50% with your spouse — or get your spouse’s signed, notarized consent to a different election or lump sum.

- Delay your retirement until after your divorce is final and you can provide the required divorce documentation.*

Source: The Retirement Group, “Retirement Plans - Benefits and Savings,” U.S. Department of Labor, 2019; “Generating Income That Will Last Throughout Retirement,” Fidelity, 2019

Survivor Checklist

In the unfortunate event that you aren’t able to collect your benefits, your survivor will be responsible for taking action.

What your survivor needs to do:

- Report your death. Your spouse, a family member, or even a friend should call your company’s benefits service center as soon as possible to report your death.

- Collect life insurance benefits. Your spouse, or other named beneficiary, will need to call Raytheon's benefits service center to collect life insurance benefits.

If you have a joint pension:

- Start the joint pension payments. The joint pension is not automatic. Your joint pensioner will need to complete and return the paperwork from Raytheon's pension center to start receiving joint pension payments.

- Be prepared financially to cover living expenses. Your spouse will need to be prepared with enough savings to bridge at least one month between the end of your pension payments and the beginning of his or her own pension payments.

If your survivor has medical coverage through Raytheon:

- Decide whether to keep medical coverage.

- If your survivor is enrolled as a dependent in your Raytheon-sponsored retiree medical coverage when you die, he or she needs to decide whether to keep it. Survivors have to pay the full monthly premium.

Life After Raytheon

Even though you might be tired and ready for a break from the demands and routine of your full-time job, it can make more sense for you financially and emotionally to carry on with your profession.

Benefits of working financially

Make up for assets' or savings' declining value. It's ideal for lump payments but more difficult to generate portfolio income due to low interest rates. Some people keep working in an attempt to offset the underwhelming returns on their investments and savings.

Perhaps you accepted a job offer from the company and left earlier than you had intended, leaving you with less money saved for retirement. You can choose to work a little bit longer to pay for things you've always denied yourself in the past rather than taking money out of savings.

Fulfill daily life expenses financially. Retirement might bring with it more expenses, so working can be a sensible and practical solution. Many workplaces offer free or inexpensive health insurance to part-time workers, so you may decide to stay working in order to maintain your insurance or other benefits.

Benefits of employment on an emotional level

When you believed you would be leaving the employment, you may find yourself having quite alluring career alternatives.

Continuing to be involved and active.

Maintaining a job—even a part-time one—can be a terrific opportunity to put the talents you've worked so hard to develop over the years to use and stay in touch with friends and coworkers.

Having fun while working.

You are under no obligation to arrange your life around the retirement age that the government has established for you through the Social Security program. Since their jobs improve their lives, many people who actually enjoy their work stay employed.

Live webinars led by seasoned financial advisors may be of interest to Raytheon who are considering retirement planning. To sign up for our next webinars specifically for Raytheon employees, call 800-900-5867.

By: John Lynch

Sources

- “National Compensation Survey: Employee Benefits in the United States, March 2019," Bureau of Labor Statistics, U.S. Department of Labor.

- “Generating Income That Will Last throughout Retirement.” Fidelity, 22 Jan. 2019, www.fidelity.com/viewpoints/retirement/income-that-can-last-lifetime .

- “Retirement Plans-Benefits & Savings.” U.S. Department of Labor, 2019, www.dol.gov/general/topic/retirement .

- AT&T Summary Plan Description, 2019

- Chevron Summary Plan Description, 2019

- Shell Summary Plan Description, 2019

- ExxonMobil Summary Plan Description, 2019

- https://seekingalpha.com/article/4268237-order-withdrawals-retirement-assets

- https://www.aon.com/empowerresults/ensuring-retirees-get-health-care-need/

- 8 Tenets when picking a Mutual Fund e-book

- Determining Cash Flow Need in Retirement e-book

- Early Retirement Offers e-book

- Lump Sum vs. Annuity e-book

- Social Security e-book

- Rising Interest Rates e-book

- Closing The Retirement Gap e-book

- Rollover Strategies for 401(k)s e-book

- How to Survive Financially After a Job Loss e-book

- Financial PTSD e-book

- RetireKit

- What has Worked in Investing e-book

- Retirement Income Planning for ages 50-6 5 e-book

- Strategies for Divorced Individuals e-book

- TRG Webinar forCorporate Employees

- Composite Corp Bond Rate history (10 years)http://www.irs.gov/retirement/article/0,,id=123229,00.html https://www.irs.gov/retirement-plans/composite-corporate-bond-rate-table

- IRS 72(t) code: https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-tax-on-early-distributions

- Missing out: How much employer 401(k) matching contributions do employees leave on the table?

- Jester Financial Technologies, Worksheet Detail - Health Care Expense Schedule

- Social Security Administration. Benefits Planner: Income Taxes and Your Social Security Benefits. Social Security Administration. Retrieved October11, 2016 from https://www.ssa.gov/planners/taxes.html

- http://hr.chevron.com/northamerica/us/payprograms/executiveplans/dcp/

- https://www.lawinsider.com/contracts/1tRmgtb07oJJieGzlZ0tjL/chevron-corp/incentive-plan/2018-02-02

-

https://www.irs.gov/newsroom/irs-provides-tax-inflation-adjustments-for-tax-year-2022

-

https://news.yahoo.com/taxes-2022-important-changes-to-know-164333287.html

-

https://www.nerdwallet.com/article/taxes/federal-income-tax-brackets

-

https://www.the-sun.com/money/4490094/key-tax-changes-for-2022/

-

https://www.bankrate.com/taxes/child-tax-credit-2022-what-to-know/